Bond Math

When people think of bonds, they often think of safety. “If I buy a CD or Treasury, I know I’m going to get my money back!” Which is true but “safety” and “stability” can be two very different things. The last few months have made that very clear. A quick refresher on what I mean.

The chart below shows interest rates at the start of the year (the red line) relative to interest rates today (the blue line). At the start of the year, three year Treasury bonds were paying 0.98%. This means if you bought a 3 year Treasury in January, you agreed to receive .98% / year. At the end of three years, you will have made 2.94% in total interest, and you will get back all the money you put in. These truths do not change due to market conditions.

However, market conditions do impact your bond’s current value at any given time.

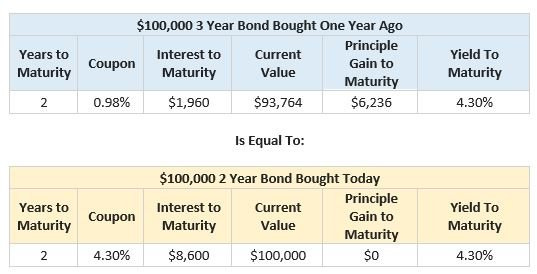

For example, using the same 3-year bond from above paying 0.98% per year, let’s say you want to sell it today. You have held the bond for one year and you have roughly two years left until you get your money back. Your bond is still paying 0.98% per year but the new 2-year bonds are paying roughly 4.3% per year. In other words, over the next two years, your bond will pay 1.96% of total interest and the new bonds will pay 8.6% of total interest. Because the new bonds will pay 6.64% more in interest over the course of the bond’s life, on your statement, the bond is now worth roughly 6% less than you paid for it.

Did I Lose Money?

Not really. If you sold your bond at a 6% loss and used the proceeds to buy a new 2-year bond paying the higher rates, you would still have profited 0.98% / year on your initial purchase amount, over the three collective years of bond ownership (excluding transaction costs and bid ask spreads.) It's like moving from the orange line, to the gray line, or the blue line. They all get you to the same place.

So will my income go up?

With fixed rate individual bonds, your income will not change immediately. For example, today’s 1-year interest rate is around 4%. If your bond has one year left to maturity and it pays 1% interest, 1% of next year’s return will come from the interest payment, while the other 3% will come from the price moving from the current statement value of approximately 97 up to 100 at maturity.

However, if you reinvest the interest payments or reinvest the principal when the bond matures, you will be buying new positions at the higher rates and that will make your income go up.

If you own a broadly allocated bond fund, there is a good chance your income will increase as the fund internally reinvests the principal as positions mature. For example, our largest bond holding is iShares Core US Aggregate Bond ETF (ticker AGG).

The fund owns 10,461 bonds with an effective duration of 6.4 years. However, it holds 60 positions maturing in the next 12 months and roughly 1,281 positions maturing in the next 24 months. That fund will constantly be buying bonds generating higher interest rates which will serve to increase the cash flow to shareholders.

We still think higher interest rates are a good thing

This note is going longer than I'd planned but if you’re still reading, thanks as always. As much as we hate seeing today’s values go down, higher interest rates make us excited for the future. In January, the 5-year interest rate was 1.2%. Had interest rates stayed there forever, our bond values would remain unchanged, but so would our income. We would have reinvested our bond proceeds at 1.2% in perpetuity and been forced to stretch for yield elsewhere.

With the 5-year interest rates now around 4.2%, our bond values are down, but our cash flow going forward is going to be higher and for most of our clients, that is a very good thing. $1,000,000 invested earning 1.2% generates $12,000 / year. That same amount invested at 4.2% earns $42,000. Once inflation subsides, the extra $30,000 / year is going to make long-term retirement planning much easier.

But what if interest rates come down?

That is a risk we hedge by not just owning the shortest bonds. By including longer bonds in our allocations, if interest rates come down, we’ll still hold bonds locked in at the higher rates. And while it will feel great to see our bond prices move higher, we’ll still have to remember the same thing we’re discussing today – your lifetime return on a bond (excluding credit issues) is generally determined when you buy it, regardless of what happens with interest rates from one day to the next.

When it comes to writing about investments, the disclaimers are important. Past performance is not indicative of future returns, my opinions are not necessarily those of TSA Wealth Management and this is not intended to be personalized legal, accounting, or tax advice etc.

For additional disclaimers associated with TSA Wealth Management please visit https://tsawm.com/disclosure or find TSA Wealth Management's Form CRS at https://adviserinfo.sec.gov/firm/summary/323123