Gold Is Not the Answer

I recently read a note from Nick Murray titled, The Persistent Illusion of Gold where cites a recent WSJ story, “When Markets Get Scary, Mom and Pop Buy Gold.” The premise of the article is that, despite all evidence to the contrary, an increasing number of people believe gold is the best place to invest:

"The percentage of Americans who believe gold is the best long-term investment jumped to 26% this year from 15% in 2022, according to a Gallup report from May. In contrast, those preferring stocks dropped to 18% from 24% last year, while those favoring bonds climbed to 7% from 4%.”

Mr. Murray’s full article is worth a read but for the purpose of this note, I’ll simply reiterate why we agree with his assessment that gold is not a good long-term investment.

1. Gold Has Been a Terrible Inflation Hedge

The primary investment thesis we hear in support of gold is that it is an inflation hedge. Unfortunately, that belief doesn’t seem to be supported by fact. For example, gold hit an all-time high in August of 2020, reaching $2,074.88 per ounce. Despite inflation rates of 4.7% in 2021, 8% in 2022, and an estimated 4% in 2023, gold lost value and, as of writing, trades around $1,950.

2. The Stock Market v Gold Has Not Been a Contest

In 1980 the S&P 500 was around 111 while gold was near $800 per ounce. At today’s level of approximately 4,500, the S&P 500 is up 40 times (ignoring the dividends it has produced along the way) vs. gold’s 2.5 times (having never produced any income). For comparison purposes, and to belabor the point made in section one, the inflation level over this same period was up 4 times.

What Should You Do If You Are Worried About Future Inflation?

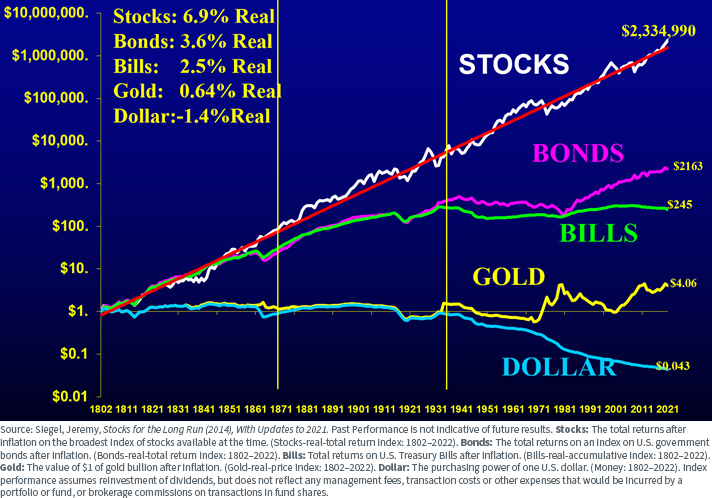

If you are looking for a long-term inflation hedge, we believe you are better off in equities rather than gold. To make the case, we can look at the real return (nominal return minus inflation) of various asset classes going back as long as possible. The above chart (which is an updated version of the chart originally appearing in Jeremy Siegel’s book, Stocks for the Long Run) compares the returns of US Stocks, Bonds, T-Bills, Gold, and Cash from 1802 – 2021. According to this study, $1 invested in US stocks in 1802 had a spending power of $2.3 million in 2021. In comparison, $1 invested in gold over that same period grew in spending power to only $4.06.

When Does Gold Make Sense?

Last week I beat up on the idea that your single-family home is a good long-term investment, but concluded by saying that you should absolutely spend money on a home that makes you happy so long as the expense is made in coordination with your financial plan. The same rule applies to gold. If you love the way gold looks and feels, you should absolutely buy jewelry and coins to the extent they make you happy. If you get peace of mind from the belief you will be able to shave bits of gold onto the grocery counter to purchase bread should the global monetary system collapse, there is certainly value in holding some physical metal. However, to the point you are justifying any gold purchase for its long-term investment value at the core of your financial plan, we strongly suggest you reconsider.

Finally, as an important reminder, we have no useful opinions as to what gold (or any other investment) will do from one day to the next. If gold were to reach new all-time highs or lows tomorrow, it would not change our long-term analysis.

When it comes to writing about investments, the disclaimers are important. Past performance is not indicative of future returns, my opinions are not necessarily those of TSA Wealth Management and this is not intended to be personalized legal, accounting, or tax advice etc.

For additional disclaimers associated with TSA Wealth Management please visit https://tsawm.com/disclosure or find TSA Wealth Management's Form CRS at https://adviserinfo.sec.gov/firm/summary/323123