Institutions Are Often Late

Occasionally I’ll see Bitcoin bulls get really excited about articles like this one from Business Insider, The State of Wisconsin Purchased $163 Million in Bitcoin ETFs in the First Quarter. The assumption being that institutional money is getting into Bitcoin and since Bitcoin has a limited supply, the price can only go higher.

But we have seen this show before.

My favorite version is from August of 1979, epitomized by BusinessWeek’s cover story, The Death of Equities.

Back then, inflation was running hot, and laws were modified to allow pensions to invest in hard assets such as gold and diamonds. When it came to diamonds the article noted that diamond dealers were jubilant and the number of banks allowing diamonds to be deposited into self-directed trust accounts was surging.

But their timing wasn’t great. From 1980 – 2000, diamond prices per carat went from $10,500 - $15,100. A 43% gain over 20 years. An annualized growth rate of approximately 1.83%.

And even if people didn’t believe in diamonds, they absolutely believed in gold. To quote the article:

Today, one of the strongest proponents of gold investing is Alaska Governor Jay Hammond. He plans to resubmit a bill to the legislature early next year to lift a law, passed in the early 1960s, that prevents the state’s public employee and teachers’ retirement funds from investing in gold, foreign securities, or real estate. At least three other states are also interested in tangibles for their retirement funds. “The statute was fine for the 1960s, but unfortunately we’re not living under those same economic conditions,” says Alaska’s deputy treasury commissioner, Peter Bushre. “We’re living under double-digit inflation, huge balance-of-trade deficits, and a serious energy problem. The current action of both the bond market and equity market bear me out.”

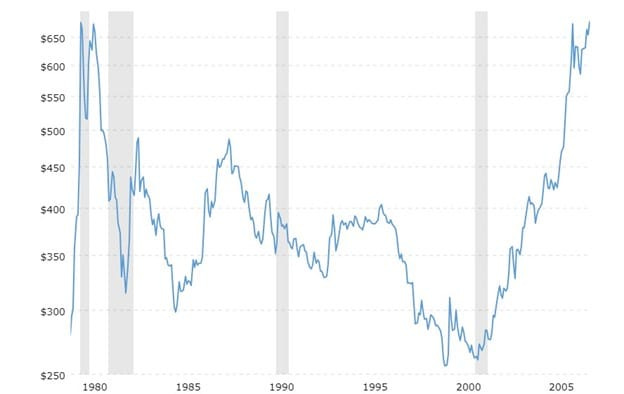

By the start of 1980, the price of gold was $594.90 / ounce. It then went plummeting lower and wouldn’t hit that value again until 2006. 26 years with zero return.

Anytime an asset class has an extraordinary run, humans fall victim to recency bias and start to believe the same things that created today's environment will persist in the future. That typically isn’t what happens. People in 1979 thought diamonds and gold were the answers. Today the same thing can be said about Bitcoin.

Even if that asset has limited supply . . . even if that asset has institutional proponents . . . even if you read about it in BusinessWeek. The price can always go lower.

P.S.

Not related to the main point of this note but another part of the BusinessWeek article I love is this one:

The problem is not merely that there are 7 million fewer shareholders than there were in 1970. Younger investors, in particular, are avoiding stocks. Between 1970 and 1975, the number of investors declined in every age group but one: individuals 65 and older. While the number of investors under 65 dropped by about 25%, the number of investors over 65 jumped by more than 30%. Only the elderly who have not understood the changes in the nation’s financial markets, or who are unable to adjust to them, are sticking with stocks.

When your younger family members say, “You just don’t get it. Things are different now.” Remember it is often those who are “unable to adjust to the changing times,” and continue to stubbornly execute on their long-term financial plans, that end up being the most successful.

When it comes to writing about investments, the disclaimers are important. Past performance is not indicative of future returns, my opinions are not necessarily those of TSA Wealth Management and this is not intended to be personalized legal, accounting, or tax advice etc.

For additional disclaimers associated with TSA Wealth Management please visit https://tsawm.com/disclosure or find TSA Wealth Management's Form CRS at https://adviserinfo.sec.gov/firm/summary/323123