Iran, Uncertainty, and Why We're Staying the Course

This week, I received a few calls and emails from clients asking whether we should increase our allocation to cash until things with Iran become less scary.

The short answer is no.

First, as we wrote about over the last few weeks, we never know what will cause the volatility, but we always expect it.

Second, while there are no facts about the future, historical evidence suggests that now is not the time to sell.

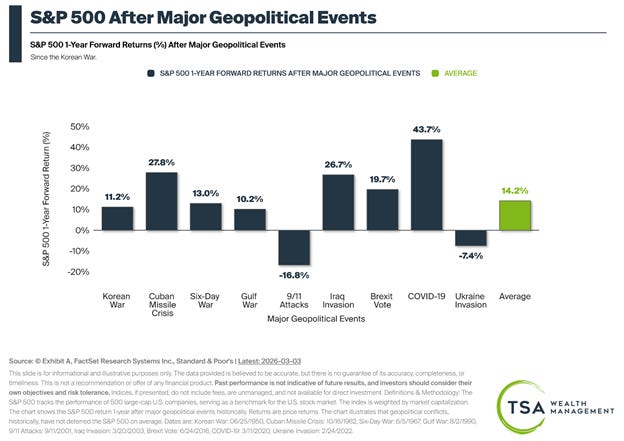

Back in 2022, after Russia invaded Ukraine (and before I published these notes to Substack), I sent out a version of this chart that went back to WWII, making the case that 83% of the time, the S&P 500 is positive one year after major geopolitical events.

Below is a consolidated version that is a little easier to read:

This is not to cheer for bad things or to minimize the potential human impact of conflict. This is simply a reminder that the world has been ending, one headline at a time, for as long as markets have existed. Successful investing requires consistency in the face of uncertainty and never reacting out of fear.

But what if this time is different?

Negative years can and will happen following a conflict. The largest negative return above was in the year following 9/11.

But context matters. The September 2001 attacks didn’t happen in a vacuum. The dot-com bubble had already begun deflating in early 2000. Corporate accounting scandals were multiplying. The economy was already fragile. 9/11 was the event that broke investor confidence in an already-stressed system.

What you’re walking into matters as much as the shock itself. A healthy economy can absorb tremendous disruption. A stretched one is more vulnerable.

Personal Note:

The tiny long-haired chihuahua we’ve been fostering has been adopted by someone in Tennessee. This dog has admittedly been one of my favorites. It has no paw on the front right, and the front left looks like a crab claw, but it still leaps with the best of them.

When it comes to writing about investments, the disclaimers are important. Past performance is not indicative of future returns, my opinions are not necessarily those of TSA Wealth Management, an SEC-registered investment advisor, and this is not intended to be personalized legal, accounting, or tax advice etc.

For additional disclaimers associated with TSA Wealth Management please visit https://tsawm.com/disclosure or find TSA Wealth Management's Form CRS at https://adviserinfo.sec.gov/firm/summary/323123