Losing Money in Bonds

In our previous note I mentioned that the stock market tends to lose value, on average, once every four years. What I failed to point out was that bonds have a similar problem. Going back to 1928, (according to this dataset from NYU) Treasury bonds have lost value approximately once every 5.2 years and Baa rated corporate bonds have lost money about once every 6.2 years.

In other words, over the course of a 30 year retirement, you should expect to see your high quality bonds generate negative annual returns 5 or 6 times. The only asset class in the data set that hasn’t lost money is the 3-month Treasury bill. But herein lies the important concept of risk and reward.

Short-term risk and long-term risk are not the same thing.

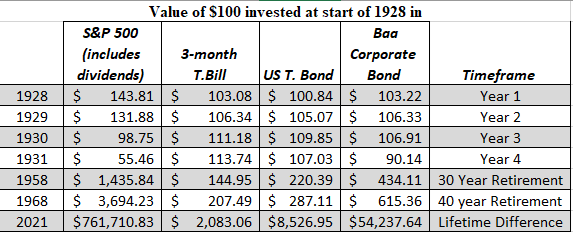

A portfolio concentrated in low risk assets, over a long period of time, has a higher risk of failure. For example, here are some numbers from the same dataset linked to above:

A hypothetical investor in 1928 that had all her money in T-bills, never had to see her account value go down. And when everything else collapsed during the Great Depression she felt very smart. Unfortunately, at the end of her 30 year retirement, her $100 investment had only grown to $144. About one tenth the amount she would have accumulated by investing in the stock market, one third what she would of have generated investing in corporate bonds, and about two thirds what she would have saved using Treasury bonds. The longer the timeframe, the larger the difference in final outcomes.

Of course, this long-term strategy only works if you are never forced to sell something when it is down. That’s why we can’t just own stocks. Retirees will always need some allocation to cash equivalents to ride out normal drawdowns as well as allocations to longer, higher returning, investment grade bonds to act as a second line of defense against protracted downturns.

Investing successfully in retirement does not require avoiding short-term losses. It simply requires the discipline to ride them out.

When it comes to writing about investments, the disclaimers are important. Past performance is not indicative of future returns, my opinions are not necessarily those of TSA Wealth Management and this is not intended to be personalized legal, accounting, or tax advice etc.

For additional disclaimers associated with TSA Wealth Management please visit https://tsawm.com/disclosure or find TSA Wealth Management's Form CRS at https://adviserinfo.sec.gov/firm/summary/323123