Should We Just Buy Short-Treasuries?

As I sit down to write, the yield on a 1-year Treasury is over 5.2%. 12 months ago, it was still around 1%. 24 months ago, it was essentially 0%.

Given this massive jump in rates, the most common question we have been hearing from conservative investors is, “Should we just buy short Treasuries?” Our answer is consistently, “No.”

If you have cash in an emergency fund and you are looking for a higher yielding option than a savings account, you should absolutely consider repositioning into short Treasuries. However, for the purpose of this conversation, I’m talking about the money you won’t need for 5, 10, 20 or 30+ years. For this portion of your portfolio, maintaining longer durations and risk exposures continues to be an important part of a healthy strategy.

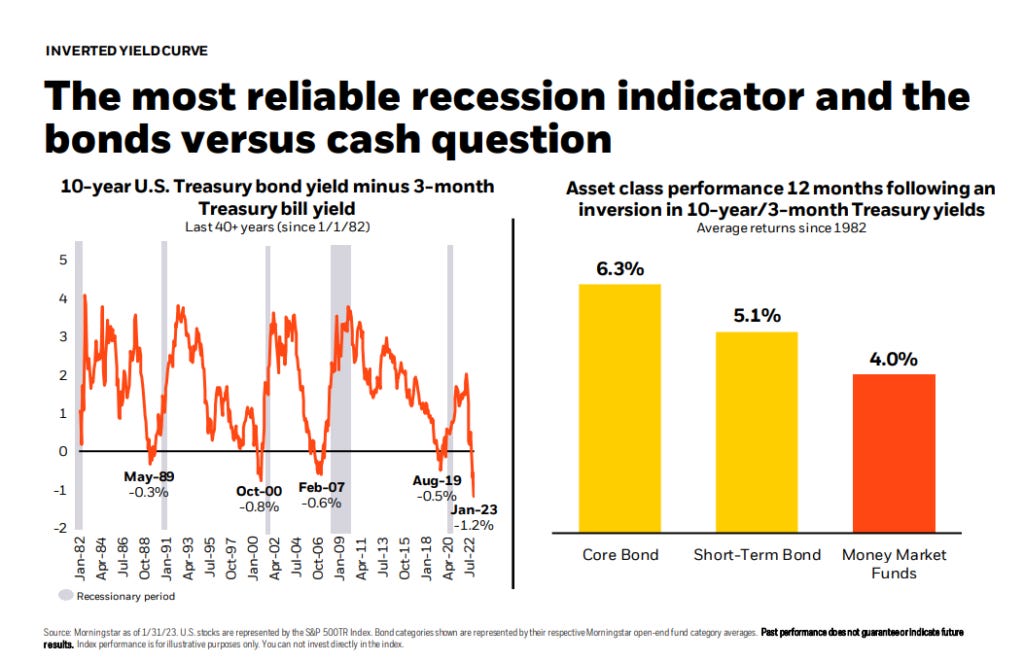

First, as the above chart points out, when the yield curve inverts (short bonds are paying higher rates of interest than longer bonds) over a 12-month period, longer term bond portfolios have historically continued to outperform despite their lower yield. This is generally because longer bonds tend to increase in price relative to shorter bonds as interest rates eventually decline.

Second, imagine you abandon your long-term portfolio and move into one-year Treasuries. What are you going to do 12 months from now if interest rates have gone back down and stocks have gone way up? Are going to go back into longer bonds when they have lower yields? Are you going to go back into stocks when their prices are already significantly higher? Or - and this is what most people do - are you going to stay in short-term Treasuries, waiting for a better time to invest? Most people end up going with the last option and their returns suffer as a result.

Finally, we always discuss the importance of consistently executing on a plan. No sound financial plan will ever be predicated on the idea that an investor will successfully jump between distinct investment strategies year after year during retirement. It is simply market timing by another name and something we need to keep far away from our long-term portfolios.

When it comes to writing about investments, the disclaimers are important. Past performance is not indicative of future returns, my opinions are not necessarily those of TSA Wealth Management and this is not intended to be personalized legal, accounting, or tax advice etc.

For additional disclaimers associated with TSA Wealth Management please visit https://tsawm.com/disclosure or find TSA Wealth Management's Form CRS at https://adviserinfo.sec.gov/firm/summary/323123