The Comfort of Not Knowing the Price

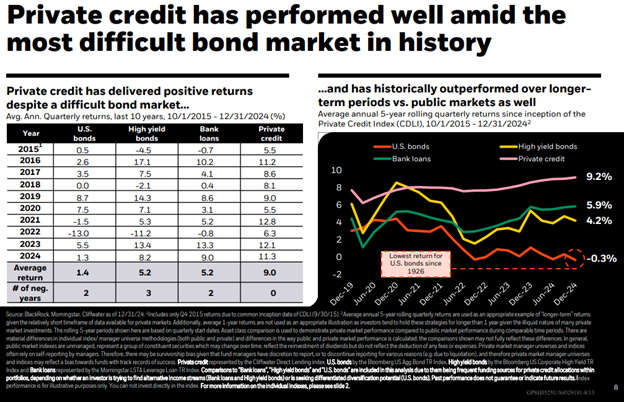

A few weeks ago, I spoke with a manager at a large private credit fund that lends to non-public companies. He was a true believer in the space and pointed to charts showing that private credit hadn’t lost money in any year over the past decade—even as the rest of the bond market has struggled.

But in light of recent headlines, I asked if he was having a hard time continuing to raise money for his private funds at net asset value (the value the company says that assets are worth), when public markets are pricing his traded funds at a 20% discount. I expected him to say things had gotten a lot harder, but he claimed they had not.

“Private investors are different,” he said. “They’re long-term and value the lack of volatility.”

In other words, people are giving private funds money to buy bonds at 100 cents on the dollar, when they could be buying the same bonds in public funds at 80 cents on the dollar just to avoid the pain of seeing price changes on their statements.

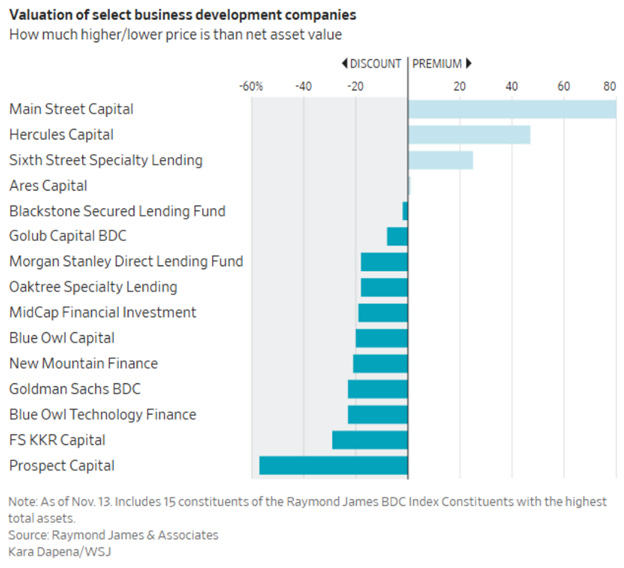

Below is a chart comparing current market values for some of the largest business development companies (private credit lenders) relative to the amounts the companies report their assets are currently worth.

A blue line -20 to the left means the company trades at a 20% discount to what it says its current portfolio is worth. From an investor's perspective, there should be no logical basis for preferring an illiquid asset (the private fund) offered at a 20% premium to its nearly identical liquid counterpart (the traded BDC).

But apparently plenty of investors do.

Because, whether they admit it or not, they like what Cliff Asness calls “volatility laundering.” The process by which money managers charge huge fees to create artificially smooth returns for what amounts to the same exposure available in the public markets.

In the year ahead, we may find that today’s stock market is wrong and the publicly traded shares of private credit companies are substantially underpriced. Or, and this is my bet, we may find that the market is right and when it comes to valuing private assets, the fund managers who most benefit from claiming high, stable valuations aren’t the best source of truth.

Either way, I look forward to seeing what happens.

A few other fun anecdotes in this category from the end of last year:

The First Brands bankruptcy. Every private credit fund that owned First Brands’ debt valued it at between 90 and 100 cents on the dollar right up until it filed for bankruptcy in September of last year.

The Blue Owl attempted merger. Blue Owl has two nearly identical private credit funds. One is traded, and one is non-traded. They attempted to merge the two, with the non-traded price at 100 cents on the dollar and the traded price at 80 cents on the dollar. It didn’t work.

Bluerock Private Real Estate’s failed listing. From 2014 through 2023, when the company was private, the price of Bluerock Private Real Estate Fund (BPRE) steadily rose, but investors had no way to access their gains. Ahead of its public listing, the fund began marking down the shares. When trading began, the company priced the shares at around $25 (down from above $40 a couple of years earlier). The market priced the shares below $15.

I guess smooth returns feel safer until the real price finally shows up.

Personal Note:

Every January 1st, I review all of our family’s expenses from the year before and update my budgets for the year ahead. My wife won’t look at the charts I put together, which is always a little disappointing, but I’m pretty sure we had this exact conversation.

HAPPY NEW YEAR !

When it comes to writing about investments, the disclaimers are important. Past performance is not indicative of future returns, my opinions are not necessarily those of TSA Wealth Management, an SEC-registered investment advisor, and this is not intended to be personalized legal, accounting, or tax advice etc.

For additional disclaimers associated with TSA Wealth Management please visit https://tsawm.com/disclosure or find TSA Wealth Management's Form CRS at https://adviserinfo.sec.gov/firm/summary/323123