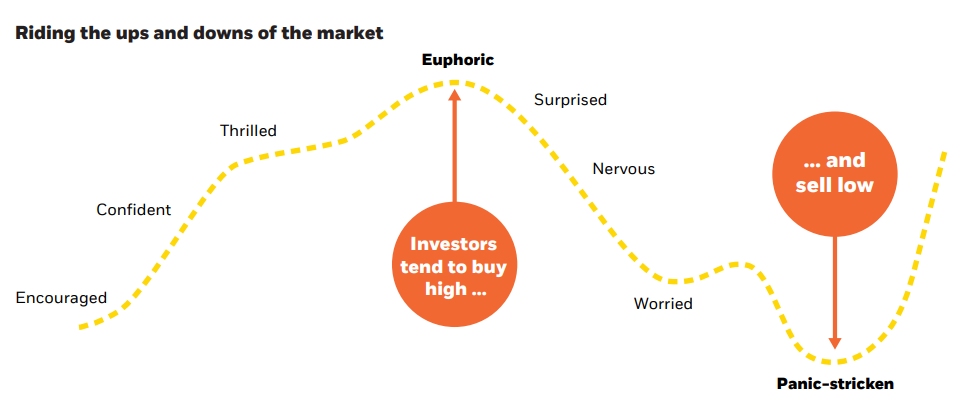

The Cost of Emotions

I cover this topic regularly throughout the year, but emotions play a huge role in determining an investor’s long-term returns. When things are good and markets are at all-time highs, investors want to buy. When things are scary and markets go down, they panic and sell. It puts them in a perpetual state of buying high and selling low.

After a few cycles of this, they get defeated, and abandon the stock market entirely.

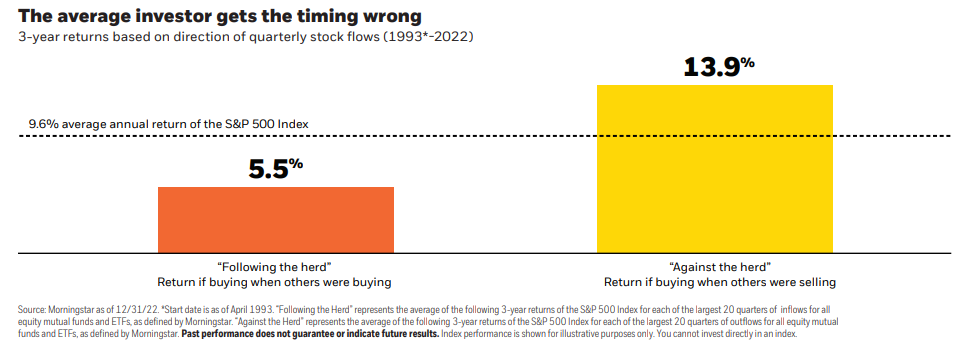

The chart below highlights the difference in 3-year returns following the periods when investors are the most confident (as reflected by fund flows into equity mutual funds and ETFs) versus when they are panic stricken (as reflected by fund flows into equity mutual funds and ETFs). This massive gap in returns is the cost of emotion.

Finally, on November 30th of last year, the CGM Focus Fund closed up shop. Since I just learned of the event, now seems like a good time to reprint an email I sent in January of last year to highlight this topic and remind you that the only thing new in the world is the history you don’t know:

On Dec. 31, 2009, Wall Street Journal published an article showing that the CGM Focus Fund was the top performing mutual fund over the previous decade, having risen by more than 18% annually. However, the typical CGM Focus shareholder lost 11% annually over that same period.

That negative 11% return isn’t a typo. From the article:

“The gap between CGM Focus's 10-year investor returns and total returns is among the worst of any fund tracked by Morningstar. The fund's hot-and-cold performance likely widened that gap. The fund surged 80% in 2007. Investors poured $2.6 billion into CGM Focus the following year, only to see the fund sink 48%. Investors then yanked more than $750 million from the fund in the first eleven months of 2009, though it is up about 11% for the year through Tuesday.”

Why am I bringing up a 12-year-old article? Because today’s funds, and their investors, have different names but all the same problems. For example, on December 13, 2021, Morningstar published this article, ARKK: An Object Lesson in How Not To Invest, which reads in part:

“Over the past five years, for example, the fund’s [ARK Innovation ETF] 41.3% annualized return places it among the top five best-performing U.S. equity funds and ETFs, and it trounced the S&P 500 (the benchmark listed in its prospectus) by more than 15 percentage points per year. After the adjusting for the timing of cash inflows and outflows, though, we estimate that investors earned less than a fourth of that return. ARKK’s estimated 9.9% investor return over the past five years lagged its benchmark by about 8 percentage points per year.”

If you take nothing else from the above, let it be this: The dominant determinant of real-life, long-term investment outcomes is not investment performance; it's investor behavior. Because while buying low and selling high is important, it is not simple. It requires controlling emotions, ignoring what is popular, and acting consistently on a plan. Most humans can’t do it, and these articles are just two very good examples.

Another fun point of follow up: I originally sent this email on 1/10/22. The ARKK fund ended up going down roughly 60% over the remainder of 2022.

When it comes to writing about investments, the disclaimers are important. Past performance is not indicative of future returns, my opinions are not necessarily those of TSA Wealth Management and this is not intended to be personalized legal, accounting, or tax advice etc.

For additional disclaimers associated with TSA Wealth Management please visit https://tsawm.com/disclosure or find TSA Wealth Management's Form CRS at https://adviserinfo.sec.gov/firm/summary/323123