The Tax Tail Wagging the Portfolio Dog

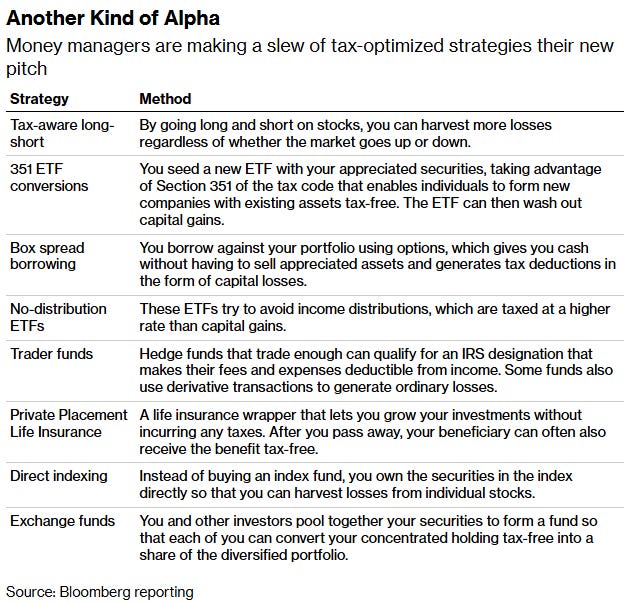

There have never been more ways to defer paying taxes on investment gains. Wall Street has made sure of that. I stole the chart below from Bloomberg, but it does a good job of explaining some of today’s tax-optimized strategies.

The menu of tax-deferral strategies has exploded in recent years, fueled by lower trading costs and better technology.

Some of these strategies work as described (direct indexing and custom indexing being strategies we regularly implement for clients), but every time Wall Street hands investors a shiny new tool to avoid taxes, they usually take it too far.

We’ve Seen This Movie Before

In the 1980s, the tax shelter industry was booming. Intangible drilling cost (IDC) deductions were a popular vehicle allowing investors to sink money into oil and gas partnerships and write off the bulk of their investment as drilling costs in the first year. The pitch was simple: save money on taxes now and maybe make money on the oil later.

For many investors, the oil never came. The deals were loaded with fees, conflicts of interest, and speculative assumptions about energy prices. When oil crashed in the mid-1980s, and Congress tightened the rules with the Tax Reform Act of 1986, investors were left holding the bag.

Real estate limited partnerships, equipment leasing deals, and movie production shelters followed the same script. The IRS eventually labeled many of them abusive and pursued investors for back taxes.

The lesson wasn’t that tax planning is wrong. It was that tax planning is never the most important thing.

The New Playbook Has Some Old Risks

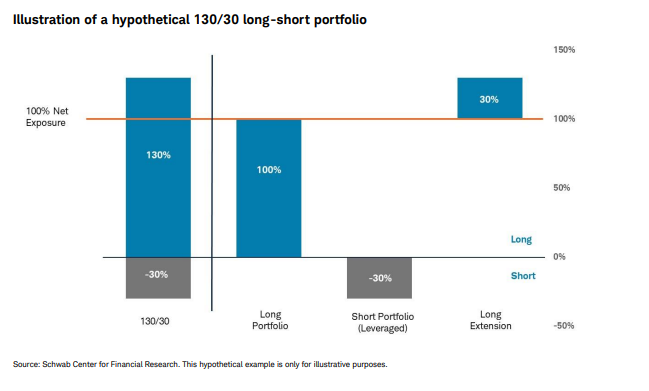

Today’s tools are more sophisticated and more transparent. Long/short strategies are one popular example.

Managers of these strategies simultaneously hold long and short positions and use leverage to create portfolios with 100% market exposure and an outsized capacity to realize capital losses for tax purposes.

But, of course, there are a couple of catches.

First, this article from Elm Wealth reviews the costs and benefits and finds that:

“The only party that is with near-certainty better off is Wall Street, while wealthy investors and the government, both individually and together, are likely worse off.”

Second, leverage has a way of converting innocuous strategies into ticking time bombs.

Custodians seem to have recognized this second point, and despite generating huge fees from the margin balances these strategies create, Schwab, Fidelity, and others are now limiting the extent to which firms can implement these leveraged long/short strategies for clients.

What Actually Works

None of this means tax planning is a waste of time. Managing the timing of gains, harvesting losses thoughtfully, maximizing tax-advantaged accounts, and being deliberate about asset location are all genuine, low-cost ways to improve after-tax returns.

However, it is important to never forget that if the underlying investment isn’t attractive on its own merits, the potential tax savings probably won’t fix it.

Personal Note:

Earlier this week, we hosted a Ladies Potting Social at The Flora Culture. My daughter attended and tells me she had a great time and loves her new plant.

The event wouldn’t have been possible without Crystal McKeon doing everything to put it together, and a huge thank you to everyone who came out and joined us.

When it comes to writing about investments, the disclaimers are important. Past performance is not indicative of future returns, my opinions are not necessarily those of TSA Wealth Management, an SEC-registered investment advisor, and this is not intended to be personalized legal, accounting, or tax advice etc.

For additional disclaimers associated with TSA Wealth Management please visit https://tsawm.com/disclosure or find TSA Wealth Management's Form CRS at https://adviserinfo.sec.gov/firm/summary/323123