This week, we hosted a seminar in our office titled Volatility & Opportunity: Managing Risk in a Shifting Economy.

Click here for a copy of the slide deck.

The presentation was divided into three sections. The first covered current market conditions. The second tried to frame the market’s recent volatility in a relevant historical context. The third discussed why solutions attempting to minimize market risk tend to do more harm than good.

Instead of reviewing all the slides, the 8-minute video above covers slides 29 – 33, briefly explaining why market volatility doesn’t have to be a bad thing.

A couple of notes:

In the video, I cite Meb Faber’s 2006 paper, A Quantitative Approach to Tactical Asset Allocation. Here is a link if anyone wants to check it out.

I forgot to add the disclaimer in the video, so here it is again.

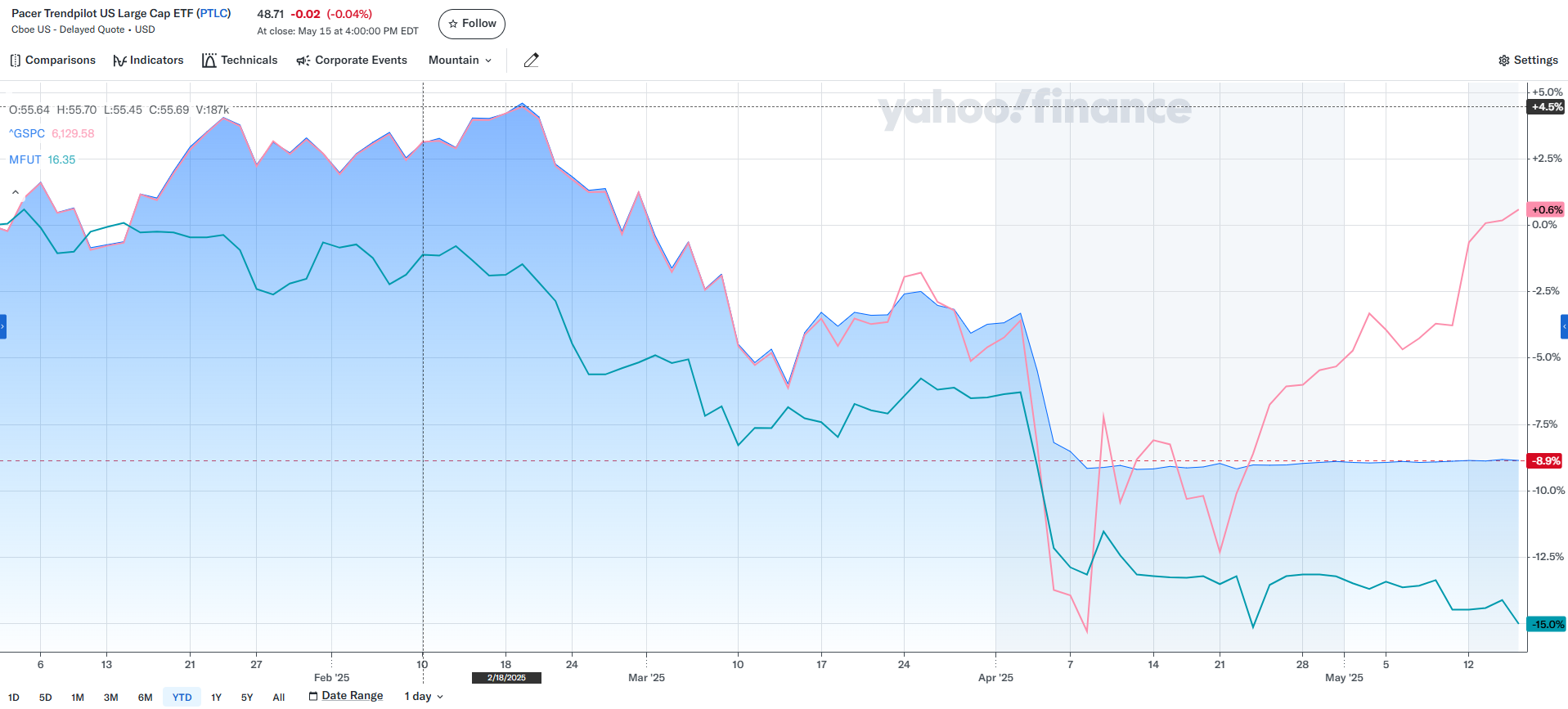

Here is an updated chart with the closing values of the funds mentioned in the video above relative to the S&P 500 as of yesterday’s close.

The S&P 500 is back to positive ground for the year, while PTLC remains in T-bills, and MFUT is still looking for the right trend.

And here is a picture from last week’s career day.

The cool thing about having a 4th grader is that he remains genuinely happy to see me when I show up at his school.