Volatility is the Price of Admission

Howard Marks recently wrote an essay, “What Really Matters?” The whole thing is incredibly good and worth a read. I could pull dozens of great quotes but for the purposes of today’s note, I’ll stick with just one:

Warren Buffett always puts it best, and on [the topic of volatility] he usefully said, “We prefer a lumpy 15% return to a smooth 12% return.” Investors who’d rather have the reverse – who find a smooth 12% preferable to a lumpy 15% – should ask themselves whether their aversion to volatility is mostly financial or mostly emotional.

- Howard Marks, "What Really Matters?" Tweet

Volatility is probably the most misconstrued concept in investing. While it is often used synonymously with risk, volatility is not risk. Volatility is simply the short-term cost of higher returns in the long run.

For most of our retiree clients, risk is properly defined as outliving one’s investments. In this context, a low volatility portfolio of short-term CDs that generate a stable 3% income, is far riskier over a multi-decade retirement than a stock portfolio subject to volatility.

Examples of Volatility in Retirement

Here is an example using a Monte Carlo analysis from the wealth management tool we use internally. In this example, a couple, ages 65 and 60, retire with about $1.6 million of portfolio assets. In the first scenario they invest in a conservative portfolio that has historically generated annual returns of 3.95% (a high quality bond portfolio with a focus on principal preservation). Assuming they both live until 90, in the upside scenario they younger spouse dies with $3 million. In the downside scenario she ends up with $1.8 million.

A very narrow range.

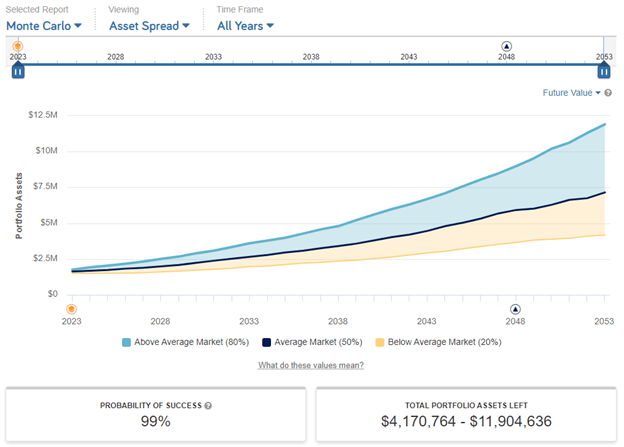

In this second scenario, with the same couple at the same starting point, the only difference is that they maintain an allocation to a portfolio more heavily weighted to equities that has projected average returns of 7.08% (approx. 70% broad based equities and 30% bonds). Now their upside scenario is $11.9 million, and their downside is $4.1 million.

No doubt a wider range with more uncertainty (they likely would have been down nearly 20% in 2022). But given a 30-year time horizon, even the worst case scenario with additional volatility is better than the best case scenario without.

Again, I’m not saying every dollar of your retirement money should be invested in the stock market. Money you may need in the next 2 to 5 years should probably be nowhere near stocks or other volatile assets. But for the long-term money, the money that will be used to fund the financial goals that extend into the lifetimes of your kids, grandkids, or charitable organizations that may exist in perpetuity, maintaining a significant exposure to volatility is the best – and oftentimes only – way to accomplish your goals.

When it comes to writing about investments, the disclaimers are important. Past performance is not indicative of future returns, my opinions are not necessarily those of TSA Wealth Management and this is not intended to be personalized legal, accounting, or tax advice etc.

For additional disclaimers associated with TSA Wealth Management please visit https://tsawm.com/disclosure or find TSA Wealth Management's Form CRS at https://adviserinfo.sec.gov/firm/summary/323123