Stories and Stocks Values

Morgan Housel has written that every forecast takes a number from today and multiplies it by a story about tomorrow. For most stocks, that means the current share price is simply today’s earnings multiplied by a story about how much those earning are going to grow in the future.

If you buy a 5% ownership interest in a company, you will be entitled 5% of the company’s future profits. The more future profits a company is expected to have, the more someone should be willing to pay for the company’s shares today.

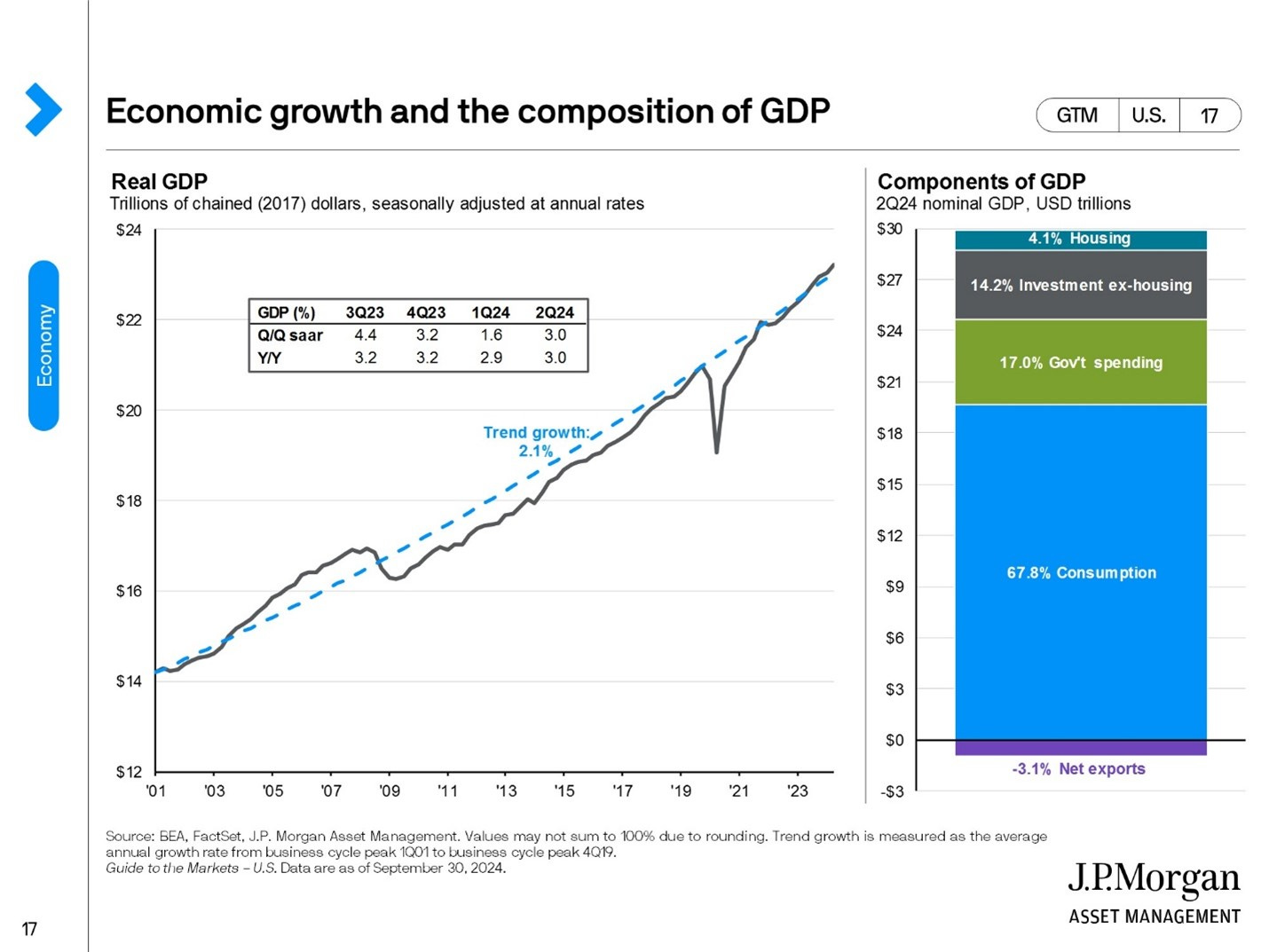

With that as our starting premise, the below chart from Carson Group’s Sonu Varghese shows how the earnings and the story multiply together to create a stock’s price:

We can break apart the price return of a stock (or index) into two components: earnings growth and valuation multiple growth (forward P/E). Note: I use forward expectations here because markets look ahead.

As of September 23, the S&P 500 price index was up 19.9% year to date, of which

· Earnings growth contributed +10.3%-points

· Multiple growth contributed +9.6%-points

As you can see in the chart [above] the volatility in the S&P 500 has come from multiples swinging wildly back and forth. Meanwhile, earnings expectations have moved steadily higher. Right now, profit growth makes up just over half the S&P 500’s year-to-date return. Contrast to two months ago, when valuations contributed the majority of the return.

The earnings growth portion of the equation is concrete. The multiple growth component represents the story about the future.

But what about changes in the economy?

As much as people talk about the economy, you would think the numbers swing wildly from one moment to the next. However, in good years our nation’s gross domestic product (GDP) may be up 3%. In a recession we may be down 1% or 2%.

The GDP difference between an ugly recession and a booming economy might be 5% whereas the price level of the S&P 500 may swing by 30 or 40% between these two scenarios.

Small changes in numbers, like those representing earnings, GDP, or consumer confidence, can make for big changes in stories.

What does this mean for investors?

Great companies with great products, can be terrible stocks if the share price reflects unrealistic expectations about the future. This happened to tech stocks in the dot com bubble and Nifty Fifty stocks in the 1970s.

Rather than simply looking at a share price and asking whether something is cheap or expensive, investors should ask, “what story is being reflected in the price?” If the story sounds too good to be true, it probably is. If the story sounds too pessimistic to be investable, it may be an opportunity.

Companies and economies don’t change much from one day to the next. But stories, and therefore share prices, can change on a dime.

—

Personal note: I’d previously mentioned being an assistant coach on my 4th grader’s football team. Here is the full squad along with some of the other, far more qualified, coaches.

A “ WINNER “ !

Uh - that would be two “ WINNERS “ ( one 🏈 )

Thanks ☕️

When it comes to writing about investments, the disclaimers are important. Past performance is not indicative of future returns, my opinions are not necessarily those of TSA Wealth Management and this is not intended to be personalized legal, accounting, or tax advice etc.

For additional disclaimers associated with TSA Wealth Management please visit https://tsawm.com/disclosure or find TSA Wealth Management's Form CRS at https://adviserinfo.sec.gov/firm/summary/323123