Why 'Smooth' Returns Should Raise Red Flags

The Trouble with Low Volatility and High Returns in Private Markets

Last week, I argued that most investors should avoid the private placement offerings being rolled out to the masses.

Around the same time, Jason Zweig made a similar case in this article from the WSJ, This New Investing Idea Isn’t Right for Your Retirement Plan: Why don’t ‘alternative assets’ like private credit belong in your 401(k)? Let us count the ways.

In the article, he writes:

That “illiquidity premium” used to be the biggest advantage of alternative investments . . . [but] when you cram illiquid assets into a liquid package, though, you negate that argument—and all kinds of weird things can happen.

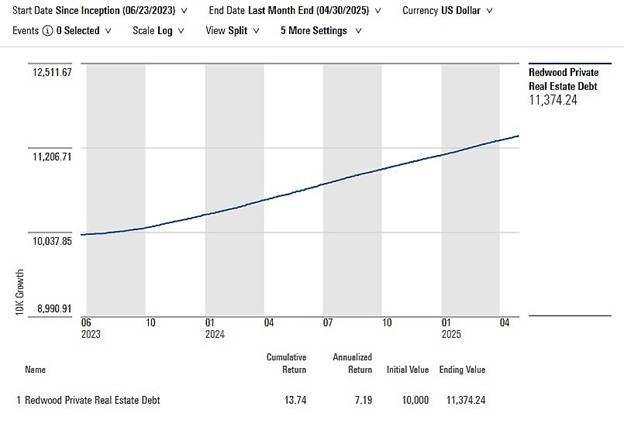

He then goes on to highlight different weird things that are currently happening using the Redwood Private Real Estate Debt Fund (CREMX) as an example.

The Redwood Private Real Estate Debt Fund is an interval fund.

Interval funds are like closed-end mutual funds in that they allow you to buy whenever you wish, but are notably different in that they only allow you to sell four times a year. Those quarterly redemptions are generally limited to 5% of the fund’s net assets. If many other people also want to get out, you might be unable to sell all (or any) of your holdings.

But this isn’t a post about why we don’t recommend interval funds. Between Zwieg’s article and this article from Morningstar, "The Unappreciated Costs and Risks of Interval Funds: The Dark Side of Incentives," I feel like that ground is pretty well covered.

Instead, this post is about charts that should make you run the other way. And interval funds create plenty of those.

For example, in a Substack post, What New Sorcery is This? Jefrey Ptak notes that the Redwood fund doesn’t have any downside volatility:

The Redwood fund incepted in June 2023 and in the time since has recorded a loss on just three days by my count—July 28, 2023 (-0.02%), Nov. 29, 2023 (-0.01%), Mar. 28, 2025 (-0.01%). On the other 460 trading days, the fund’s value was either unchanged (181 days) or it notched a gain (279 days).

And as amazing as that sounds, of the 79 other interval funds out there, 7 had higher Sharpe ratios, meaning they showed essentially the same non-existent volatility but with even higher average returns.

But there are no free lunches.

You cannot apply leverage to high-yield debt to amplify returns like these interval funds do without amplifying the volatility.

But we have seen this before.

For example, in a seminar I gave last year, I asked, " Which of these investments would you rather own?"

For most people, the orange line seemed too risky, the yellow line didn’t grow fast enough, and why would anyone want the green line instead of the pink?

Then I revealed the names along with what happened next.

The orange line represented Pfizer stock, the green line represented the S&P 500, the yellow line represented US Treasury Bills, and the pink line represented Fairfield Sentry, a feeder fund for Bernie Madoff’s hedge fund.

This isn’t to say today’s interval funds are Ponzi schemes. But if something looks too good to be true, it probably is.

When the market for these investments turns south and investors request their money back, they may be disappointed to learn that these investments were, in fact, much more volatile and less liquid than they were led to believe.

Personal note:

For Memorial Day weekend, we went down to Bolivar to do some shark fishing from the beach. We didn’t catch any sharks, but it was still fun, and the kids are now on summer break.

Next week they go off to camp.

When it comes to writing about investments, the disclaimers are important. Past performance is not indicative of future returns, my opinions are not necessarily those of TSA Wealth Management, an SEC-registered investment advisor, and this is not intended to be personalized legal, accounting, or tax advice etc.

For additional disclaimers associated with TSA Wealth Management please visit https://tsawm.com/disclosure or find TSA Wealth Management's Form CRS at https://adviserinfo.sec.gov/firm/summary/323123